The AI Corner

BREAKING: SpaceX just offered $60 billion for Cursor. The FTX ghost makes it stranger

Ruben Dominguez

Apr 22, 2026

BREAKING: SpaceX just offered $60 billion for Cursor. The FTX ghost makes it stranger

Source: The AI Corner — Author: Ruben Dominguez — Date: April 22, 2026 — Original article

The opening hook: a $200,000 ghost

In April 2022, Alameda Research (the for-profit trading arm tied to Sam Bankman-Fried's FTX empire) wrote a $200,000 check into a four-person startup nobody had heard of. The startup was building a CAD tool for mechanical engineers. That check bought roughly 5% of the company at a ~$4 million post-money valuation.

When FTX collapsed in November 2022, the stake became part of the bankruptcy estate run by John Ray. In April 2023, Ray sold it for $200,000 — exactly cost basis, zero gain.

On April 21, 2026, SpaceX announced it had the right to acquire that same company for $60 billion. The undiluted Alameda position, had it survived, would be worth roughly $3 billion today.

The company is Cursor. This piece is the breakdown.

Four MIT kids and the fastest revenue curve in software history

Michael Truell, Sualeh Asif, Arvid Lunnemark, and Aman Sanger graduated from MIT in 2022 and started building immediately. Their path:

- A CAD tool for mechanical engineers

- A short detour through text-to-image

- An AI-native code editor, shipped publicly in March 2023

The pivotal product decision was building Cursor as a full fork of VS Code rather than as an extension on top of it. This matters because extensions are constrained by what the host editor's API exposes — you can only do what Microsoft lets you do. A full fork lets you rewrite the UI from scratch, intercept keystrokes anywhere, restructure the editing surface, and ship features extensions literally cannot. That's why competitors couldn't catch up to Cursor's UX even after copying ideas.

What followed was a revenue ramp without a real precedent in software:

| Milestone | Date |

|---|---|

| $1M ARR | October 2023 |

| $100M ARR | January 2025 |

| $500M ARR | June 2025 |

| $1B ARR | November 2025 |

| $2B ARR | February 2026 |

| $6B ARR (guided) | End of 2026 |

The $1M → $100M leg took 12 months. For comparison: Wiz took 18, Deel 20, Ramp 24. Cursor is the new benchmark.

The team is roughly 150–200 employees. At $2B ARR that puts revenue per employee near $10 million, among the highest ratios in software history.

A few other numbers worth holding in your head:

- 7M+ monthly free users

- 1M+ paying individual developers

- 50,000+ paying teams

- ~70% of the Fortune 1000 as enterprise customers

- Enterprise revenue went from 25% of the mix in late 2024 to 60% by February 2026

"My favorite enterprise AI service." — Jensen Huang, CEO of NVIDIA

In Stack Overflow's 2025 Developer Survey (49,000+ respondents), Cursor registered 18% usage in its first year of inclusion — the fastest IDE adoption in software history. Claude Code registered 10%.

The funding ladder

| Round | Date | Amount | Valuation | Lead |

|---|---|---|---|---|

| Pre-seed | Apr 2022 | $400K | ~$4M | Neo, Alameda, Heroic |

| Seed | Oct 2023 | $8M | — | OpenAI Startup Fund |

| Series A | Aug 2024 | ~$60M | $400M | a16z + Thrive |

| Series B | Dec 2024 | $100M | $2.6B | Thrive Capital |

| Series C | Jun 2025 | $900M | $9.9B | Thrive Capital |

| Series D | Nov 2025 | $2.3B | $29.3B | Accel + Coatue |

| Series E (in talks) | Apr 2026 | ~$2B | ~$50B pre | a16z + Thrive |

Two things to notice:

First — OpenAI was the first institutional investor. They tried to acquire Cursor twice. Got rebuffed both times. Settled for Windsurf at $3 billion (a saga we'll come back to). Now Musk is offering $60 billion for the company OpenAI discovered first — 7.5× the Windsurf price — six days before jury selection in Musk v. Altman.

Second — Thrive Capital appears in four consecutive rounds. That's not normal.

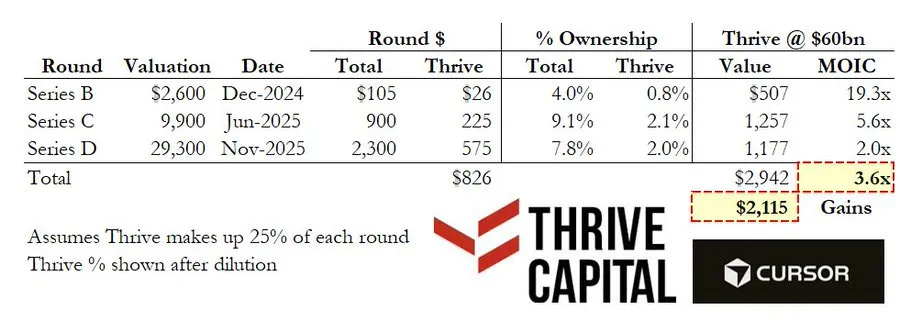

What real conviction looks like: Thrive Capital

Most investors got one shot at Cursor. Thrive took three.

- Series B at $2.6B valuation — led the round

- Series C at $9.9B — led again

- Series D at $29.3B — co-led

Three consecutive rounds. Increasing check sizes. Increasing conviction across 24 months.

If SpaceX closes at $60B, the math (after dilution, assuming Thrive took ~25% of each round):

- Series B: $26M in → 0.8% post-dilution → ~$507M → 19.3x MOIC (multiple on invested capital — i.e., return per dollar)

- Series C: $225M in → 2.1% → ~$1.257B → 5.6x

- Series D (closed only six months ago): $575M in → 2.0% → ~$1.177B → already a clean 2x

- Blended: 3.6x on ~$826M invested

- Total gains: over $2 billion

This is what differentiated venture investing looks like in practice — not finding the company once, but reading the curve correctly each subsequent round and pressing the bet when the price went up. The author flags an open question: Thrive is now deploying a new $10 billion fund. Cursor proves concentrated conviction can still produce extraordinary returns at smaller fund sizes; whether the math survives at $10B is a separate question.

The SpaceX deal: what it actually is

The April 21 announcement is a call option, not a closed acquisition. (A call option = the right, but not the obligation, to buy at a set price by a set date.)

The structure:

- SpaceX has the right to acquire Cursor for $60 billion later in 2026.

- If SpaceX walks away, it pays Cursor $10 billion for joint work on Composer (Cursor's in-house inference model).

- Cursor granted SpaceX 12 months of acquisition exclusivity.

CEO Michael Truell's response on X was deliberately understated:

"Excited to partner with the SpaceX team to scale up Composer. A meaningful step on our path to build the best place to code with AI."

Cursor's official blog post made no mention of the acquisition option or the $10B alternative. It framed the deal purely as a compute partnership. That editorial choice signals how seriously they are taking the independence narrative — they want to keep the option to stay independent open, both legally and in employees' and customers' heads.

The timing is pointed: jury selection in Musk v. Altman begins April 27 — six days after the announcement. Musk is locking up the asset OpenAI discovered first, at 20× the price of OpenAI's comparable acquisition (Windsurf), in the same week he takes Altman to trial.

Why this deal makes sense for both sides

For SpaceX:

SpaceX filed confidentially for IPO on April 1, targeting roughly $1.75 trillion. The problem is the IPO story is mostly speculative hardware — and one of the SpaceX-adjacent assets, xAI, lost $6.4 billion in 2025. Cursor brings $2B in real ARR and 70% of the Fortune 1000 into the IPO narrative — commercial ballast for a vehicle built around long-cycle hardware bets.

xAI also publicly admitted Grok "is currently behind in coding" and was "not built right first time around." Back in March 2026, xAI had already hired two senior Cursor product-engineering leads, both reporting directly to Musk. The April announcement was visible from miles away.

For Cursor:

The Windsurf saga (next section) showed the existential risk of depending on frontier-lab models. Cursor's core models are Claude, GPT, and Gemini — supplied by Anthropic, OpenAI, and Google, all now competing with Cursor directly via Claude Code, Codex, and Jules. The supplier is the competitor.

The SpaceX option gives Cursor three things:

- A $10B floor even if the deal breaks

- Guaranteed compute for training Composer at a scale frontier labs would never sell to a direct competitor

- Leverage against the API-cutoff risk that destroyed Windsurf's independence

And critically — Cursor is running a $2B round at a $50B pre-money valuation in parallel. You only do that when you have options, not when you have already decided to sell.

The Windsurf saga: why this matters

A short timeline that explains the whole strategic backdrop:

- April 2025: OpenAI agrees to acquire Windsurf (Cursor's main competitor) for $3B.

- During exclusivity: A Microsoft IP dispute stalls the deal. Anthropic cuts off Claude API access to Windsurf — punishing the deal in real time.

- July 11, 2025: Exclusivity expires.

- Within hours: Google announces a $2.4B reverse-acquihire of the Windsurf founders into DeepMind. (A "reverse-acquihire" = buy the people, leave the company shell behind.)

- Three days later: Cognition acquires the remaining husk of Windsurf — IP, brand, $82M ARR, 350 enterprise customers — for roughly $250 million.

The lesson: any coding tool dependent on frontier-lab APIs is permanently exposed to the labs using API access as a weapon. Cursor saw this clearly before it happened to them. Composer, their proprietary inference model, is the strategic response — and the SpaceX deal is what makes Composer trainable at scale.

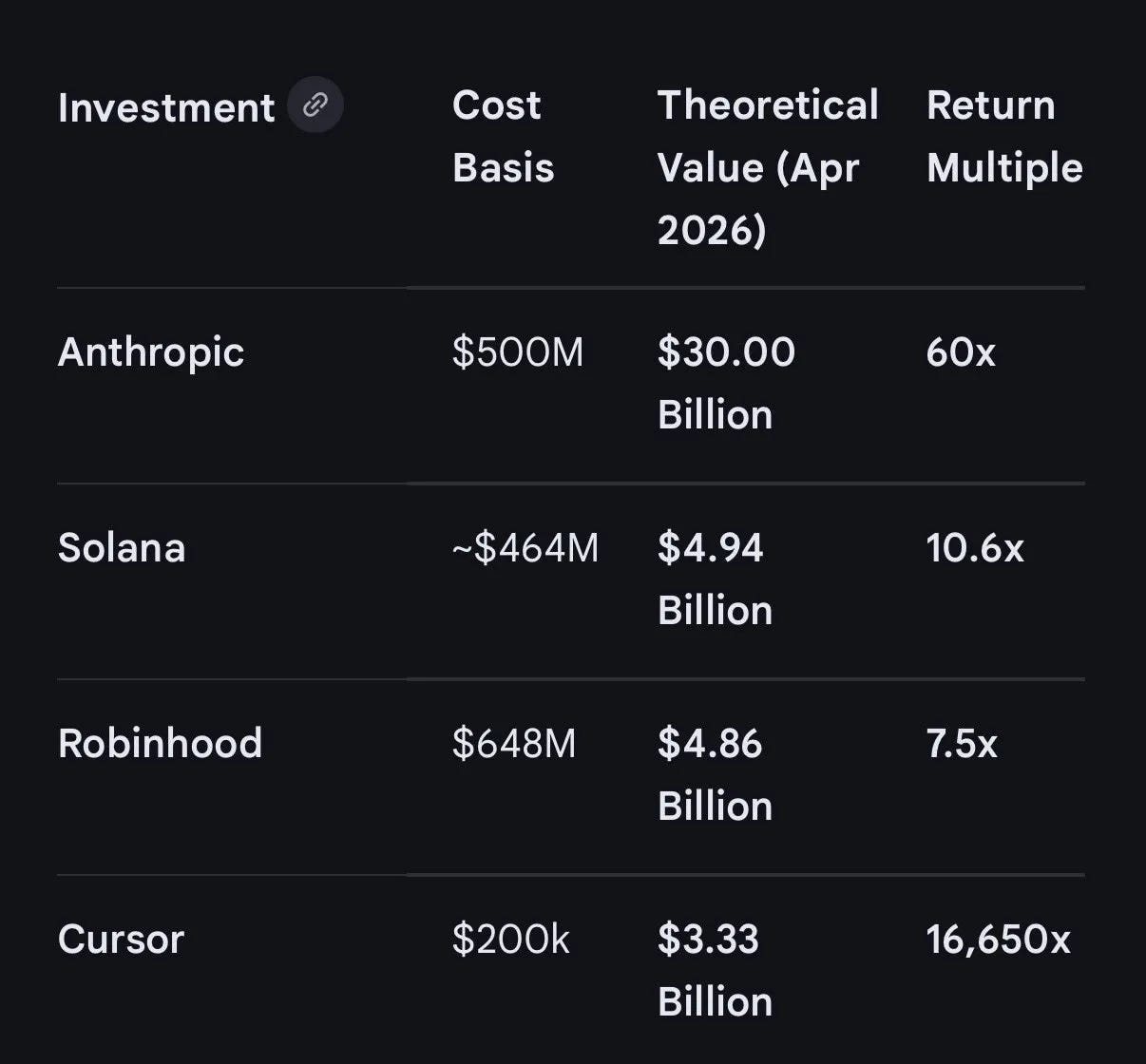

The FTX ghost

The Alameda investment came through Clifton Bay Investments LLC, the FTX Group's for-profit venture arm. $200,000 in April 2022. ~5% of Cursor at a ~$4M post-money.

When FTX collapsed in November 2022, that stake became an asset of the bankruptcy estate under John Ray. In April 2023, Ray sold it for $200,000 — cost basis. The buyer has never been publicly identified.

The undiluted counterfactuals at each subsequent valuation:

- ~$450 million at the May 2025 $9B valuation

- ~$1.47 billion at the November 2025 Series D

- ~$3 billion at SpaceX's $60B option price

Real dilution would shrink those numbers, but the order of magnitude holds.

The chart pulls out four FTX-era positions:

- Anthropic: $500M cost basis → ~$30B theoretical → 60x

- Solana: ~$464M cost basis → ~$4.94B → 10.6x

- Robinhood: $648M cost basis → ~$4.86B → 7.5x

- Cursor: $200K cost basis → ~$3.33B → 16,650x

Had the FTX estate held its AI and crypto positions, the theoretical portfolio value today would be $52–86 billion. Ray sold the Cursor stake at cost in April 2023 and the Anthropic stake for ~$1.3B across 2024 — at Anthropic's February 2026 valuation of $380B, that Anthropic position alone would now be worth roughly $30B.

A widely-shared post on X after the announcement put it sharply:

"So you're telling me SBF did Anthropic, Cursor, Solana and Robinhood? His NAV would've been about $52–86 billion today. 9.8–16.2x TVPI." — @JasonrShuman

(TVPI = Total Value to Paid-In, a standard fund-return metric.)

The author is careful here: the math does not vindicate Bankman-Fried. Customer funds were misappropriated; that's a fact of fraud, not portfolio construction. But it does complicate the story — the bankruptcy estate's job was to convert assets to cash quickly, and in doing so it sold what would become some of the defining venture positions of the AI era.

One more notable detail: Anysphere (Cursor's parent company) has never publicly acknowledged the Alameda backing in any press release, funding announcement, or blog post.

What happens next

Two scenarios.

If SpaceX exercises at $60 billion:

- Cursor becomes Musk infrastructure.

- Anthropic and OpenAI accelerate their own IDE plays.

- Fortune 500 companies with data-sovereignty concerns start re-evaluating (Cursor under SpaceX is a different vendor profile than independent Cursor).

- The Musk consolidation arc completes: X → xAI → SpaceX → Cursor → IPO.

If the option lapses:

- Cursor pockets $10B in compute resources.

- Closes its $50B independent round.

- Becomes a serious IPO candidate — potentially the first standalone AI-native software company to reach public markets at scale.

The author reads Cursor's behavior right now as the second scenario. A $2B parallel fundraise at a $50B pre is not how a company acts when it has already decided to sell.

The closing thread

The FTX angle is the story's emotional core. A $200,000 check from a company that became synonymous with fraud bought what would have been one of the most valuable venture positions of the decade. The estate sold it at cost to move fast. Three years later, Elon Musk is offering $60 billion for the same company — six days before taking Sam Altman to trial.

The bill for that haste, if SpaceX exercises, reads at roughly $3 billion undiluted.

Author

Ruben Dominguez

Continued reading

Keep your momentum

MKT1 Newsletter

100 B2B Startups, 100+ Stats, and 14 Graphs on Web, Social, and Content

This is Part 2 of MKT1's three-part State of B2B Marketing Report. Where Part 1 looked at teams and leadership , Part 2 turns to what marketing teams are actually doing — what their websites look like, how they use social, and what "content fuel" they're producing. Emily Kramer u

Apr 28 · 10m

Lenny's Newsletter (Lenny's Podcast)

Why Half of Product Managers Are in Trouble — Nikhyl Singhal on the AI Reinvention Threshold

Nikhyl Singhal is a serial founder and a former senior product executive at Meta, Google, and Credit Karma . Today he runs The Skip ( skip.show (https://skip.show)), a community for senior product leaders, plus offshoots like Skip Community , Skip Coach , and Skip.help . Lenny de

Apr 27 · 7m

The AI Corner

The AI Agent That Thinks Like Jensen Huang, Elon Musk, and Dario Amodei

Dominguez opens with a claim that is easy to skim past but worth stopping on: the difference between elite founders and everyone else is not raw IQ or speed — it is that each of them has internalized a repeatable mental procedure they run on every important decision. The procedur

Apr 27 · 6m